by California Casualty | Safety |

Hurricane season is upon us, after a violent spring storm season. Hopefully, we’ve seen the worst of the severe weather for the year, but it pays to be prepared.

The NWS National Hurricane Center has some great resources for learning more about hurricanes, their dangers, and safety precautions you should take.

It will help you identify the main questions you need to be able to answer if you are in a hurricane prone area:

- What are the Hurricane Hazards?

- What does it mean to you?

- What actions should you take to be prepared?

You should also consider calling your insurance agent or customer service department to make sure you have the appropriate coverage in case disaster strikes!

by California Casualty | Helpful Tips |

Planning a night out or a fun day without the kids? Make sure your babysitter is ready for more than just snacks and bedtime stories. Prepare them with the right information to handle any situation—whether it’s a scraped knee, a tantrum, or a power outage. When they’re prepared, you can truly relax.

Having a clear, written plan for your babysitter is essential for peace of mind. In unfamiliar or stressful situations, even the most experienced sitter might forget key details. A written guide provides them with easy access to the important information they need to stay calm and handle things efficiently.

Family Information

Your sitter may know you well or may be meeting you for the first time. Either way, it’s good to provide the basics in case they need to reference the information, whether it’s for a pizza delivery or a 9-1-1 call.

- Home address (and nearby cross streets or landmarks if needed)

- Full names and ages of each child

- Home phone landline (if there is one)

- Your cell phone number

- Name and number of a neighbor, close friend or relative as a backup

Pro Tip: Get your sitter to program your cell phone number into their phone before you leave.

Emergency Contacts

Emergencies happen, and when help is needed right away, your sitter may have to call 9-1-1. Share examples of when they should do so, such as when someone is injured beyond the first aid they can provide, or if a child has been exposed to a potentially toxic substance. If there’s a fire in the house, they still need to call, but they should leave the home first with your child(ren) and call from outside.

- Poison Control Center (800) 222-1222 (open 24/7)

- Pediatrician’s phone number (which will connect to after-hours care)

- 9-1-1 (police and fire)

In case of fire, share these instructions with the sitter:

- Do not try to put the fire out yourself.

- Bring the children out of the house. Do not go back in for any reason, even to rescue pets.

- Call 9-1-1. Stay on the line until the operator says it is okay to hang up.

- Call the parents after you have called 9-1-1.

- Wait at a safe distance with the children.

In case of severe weather, use this as your basis for instructions to the sitter:

- In a hurricane, tornado or high-wind storm, stay inside your home. Choose a small, interior room without windows, such as a bathroom or closet, on the first level.

- Share the location of flashlights, extra batteries, candles and matches in case the power goes out. (They can also use the flashlight on their phone.)

- Call the parents to let them know. Conserve your phone’s battery so you can stay in communication.

Medical Information

Whether it’s allergies, medications, or any existing health conditions, providing this information ensures the sitter is prepared to act quickly and appropriately.

- Food and medication allergies (if any) listed for each child

- Where medicine is stored, instructions on how and when to administer (and whether they need your permission to receive)

- Location of the first aid kit, band-aids and other medical supplies

- A healthcare authorization form in case you can’t be reached in an emergency and your child needs medical care (You can find these forms online.)

Schedule & Routines

Think through a typical day and write down the routines for your children. Use that as a basis for the schedule you will provide for your sitter.

- Include approximate times, as it may take longer than usual when a person other than you is directing.

- Chores or homework for which the kids are responsible

- Essential supplies (e.g. a lovey and sound machine for bedtime)

- Include options for discipline (e.g. loss of screen time) and rewards (e.g. an extra story) to help encourage children to follow the routine.

Snacks & Meals

Whether or not your sitter will be feeding your child, they will likely have to negotiate requests for snacks.

- Establish the rules on snacks and sweets, and when children can have them.

- Make sure your sitter knows what is safe for a baby or toddler to eat. Don’t give a child under age 4 whole grapes, whole hot dogs, hard candy, popcorn, or other choking hazards.

- Plan to feed your sitter if they are there during mealtime and let them know the options.

Safety Rules

Safety isn’t always commonsense. Make sure your sitter is aware of the following rules.

- Never leave child unattended in a bathtub or on a high surface like a changing table.

- Keep children away from windows.

- Don’t let little ones play near stairs.

- Don’t allow children to play with household appliances or dangerous objects, including plastic bags which can present a suffocation hazard.

- Never leave children alone with a dog, even the family dog. Bites can happen quickly and unexpectedly even with a pup that hasn’t bitten before.

- Never leave the children alone in the house.

- Avoid swimming pools and trampolines when the parent is not around.

House Rules

You will want to share your rules about what is allowed, from screen time to what the sitter is allowed to do when the kids are asleep. Here are some rules to consider.

- How much screentime children are allowed

- Whether the sitter is allowed to post photos of your kids on social media

- What is off-limits in terms of television shows (even when kids are asleep), technology, food and drinks

- Your policy on visitors (e.g. no friends, don’t open the door unless the parent has let you know that a visitor is expected)

- No sleeping on the job

When Your Babysitter Arrives

- Ask your sitter to arrive 15-30 minutes before you plan to head out to allow ample time for instructions. It’s worth the additional peace of mind to pay her for this extra time.

- Give your babysitter a tour of the house if she or he hasn’t been there before. Point out any areas that are off-limits to the sitter and/or the kids. Show him or her two ways out of each room in case of a fire.

- If you have Nanny cams, point them out.

- Go over the written instructions and leave them posted in a visible, easily accessible place, such as stuck to the fridge with a magnet.

- Give your sitter a chance to ask questions.

- Confirm your expected arrival back at the home and let them know how you will update them if you are running late.

- Enjoy your day or night out with the peace of mind that you’ve taken the steps to keep everyone safe.

This article is furnished by California Casualty, providing auto and home insurance to educators, law enforcement officers, firefighters, and nurses. Get a quote at 1.866.704.8614 or www.calcas.com.

by California Casualty | Finances, Helpful Tips |

Imagine finding a contractor to repair your roof after a damaging storm, only to discover that you’ve been duped by a scammer. It’s a situation no one wants to face, yet contractor scams are on the rise, leaving unsuspecting homeowners with unfinished projects and empty wallets. Before you embark on your next project, whether it’s a home renovation or repairs following a disaster, it’s important to know the warning signs so you don’t become the next victim.

What exactly is a contractor scam?

You expect a contractor to provide professional repairs or updates to your home. However, when they make promises but they don’t deliver on them, that’s a scam. They intentionally mislead you. They might do a job that is substandard, overly expensive or they may not do the job at all. If your area is hard hit by a wildfire, tornado, hurricane, extreme weather or other disaster, be aware. Scammers posing as contractors may try take advantage of the situation.

Types of Scams

Pushy, door-to-door contractors

Beware of contractors who show up at your door, unsolicited. That’s the first red flag. When they are high-pressure salesmen, you know something is wrong. They can be very convincing, but don’t fall for discounts that only apply if you hire them on the spot. If you didn’t ask for their quote, chances are they are not the right contractor for you.

Out-of-state contractors

Some contractors chase storms to look for easy money. Be suspicious of anyone out-of-state who is offering a quote on work. Be especially careful of contractors working out of their vehicle rather than an office. An out-of-state contractor can be hard to contact if you have issues or work isn’t completed. Choose a local contractor instead.

Unlicensed and uninsured

Scammers may tell you they don’t need to be licensed to do the work. That’s not the case. Your state likely has requirements a contractor must meet. They need to be licensed, and they should be able to show you a license from the state contractor’s board. Double check the number that they show you with the board; scammers can sometimes present inactive licenses. A contractor should also have proof of insurance. If they don’t, that means you could be paying for expensive mistakes that they make.

No references and/or bad reviews

Ask for photos of previous work and customers you can contact. If a contractor cannot provide that, then it’s likely they are not legitimate. Also do a search online for the contractor’s name along with the word “scam” or “complaint.” Read the reviews. Check with the Better Business Bureau to see if there are complaints filed. You might find reasons not to hire this contractor.

No written contract

You should know in writing what work will be done for what price. When contractors don’t provide a written contract before work starts, that’s not professional. You should always thoroughly read the contract, including the fine print. Don’t sign it if you have any concerns. Never sign a blank contract.

Payment requires in full at the start

Don’t deal with a contractor who asks for payment in full upfront. Sometimes contractors require a deposit, but full payment should never be provided before work is done. Know that you can negotiate a reasonable downpayment; some states even limit how much that can be. Contact your state consumer protection agency to find out more.

Unusual forms of payment

Beware of payment requests for wire transfers, gift cards, payment apps, insurance checks, cryptocurrency or cash. Don’t borrow money from a lender they know. Scammers love these types of payments because they are almost impossible to get back. Beware of scammers who offer to help you qualify for FEMA relief for a fee. FEMA doesn’t charge fees, and you are better off doing that on your own.

Cost quotes on places you cannot see

Don’t let an unknown contractor inspect your roof and then tell you what must be done. Ask for pictures of places you cannot easily access, such as crawl spaces, ducts, your roof, etc. Then verify that those images are of your home. If it is a cost quote on an area that you cannot see, get several quotes from those you trust.

Promise of immediate repairs

If something sounds too good to be true, it probably is. Don’t believe a contractor who promises immediate repairs. There’s usually a timeline for quality work. Make sure the contractor you choose doesn’t cut corners by skipping steps to get repairs done right away.

Frequent unexpected expenses

Whenever there’s a construction repair job, there’s a chance of unexpected expenses. Your contractor may find mold, for example, when they work on your home. However, when there are frequent unexpected expenses or expensive ones, get a second opinion. You may find that these unexpected expenses aren’t real ones at all.

Low-grade materials

Make sure the material listed on the estimate is the material being used. Contractors can switch out low grade materials to save money and sacrifice quality.

No one on the job

If no one is on the job during working hours, that’s a big red flag. It could be that your contractor is using subcontractors that arrive after their day jobs. Or it could be that no one will show up to do your work at all.

Protect Yourself from Scams

You can take precautions to help prevent falling victim to a contractor scam. Here are some guidelines.

- Contact your home insurer. When your home is damaged from extreme weather or other disasters, your insurer will need to survey the damage before you get it repaired. They will help you prepare a claim and identify reputable contractors. Before you hire anyone, verify your insurance coverage. Don’t rely on a contractor to tell you what is covered.

- Get multiple quotes from local contractors. That way you’ll know if the price is in the ballpark. Remember that the lowest bid is not always the best. That contractor may be cutting corners. Also make sure you are comparing apples to apples. Pro Tip: use the BBB Get a Quote tool at https://www.bbb.org/get-a-quote.

- Do your research. Check references and ask for photos. Verify your contractor’s license and insurance. Read online reviews and look up your contractor on the Better Business Bureau.

- Get a written contract. Make sure it includes the contractor’s name, address, phone, license number, an estimated start and finish date, a payment schedule, the scope of work and cost of labor and materials. Make sure it also includes a written statement of your right to cancel the contract within three business days if you signed it in your home or in a location other than the contractor’s permanent place of business. Make sure it has no blank spaces that a contractor could fill in later.

- Guard your money. Never pay a deposit that is more than 25% of the total cost and never pay anything until materials are delivered to your home. Don’t sign over insurance checks to contractors. If you have any questions, contact your insurance agent. Don’t make the final payment until the job is complete.

- If you suspect a scammer, report them. You can report scams to the Better Business Bureau, the National Center for Disaster Fraud, and the Federal Emergency Management Agency (FEMA). You can also consult StopFraud.gov.

Your home is one of your greatest investments. Make sure it is covered with the right insurance.

This article is furnished by California Casualty, providing auto and home insurance to educators, law enforcement officers, firefighters, and nurses. Get a quote at 1.866.704.8614 or www.calcas.com.

by California Casualty | Helpful Tips, Travel |

Get your gear ready. It may be winter, but it’s a great time to go camping. Not only will you find comfortable temperatures, but you’ll also enjoy spectacular scenery, lower costs, and fewer crowds. Here are some of our favorite destinations for winter camping.

ARIZONA

Twin Peaks Campground

https://www.nps.gov/orpi/planyourvisit/twin-peaks.htm

Sonoran Desert, Arizona (2 hours from Phoenix)

Cost: Starting at $20 per night plus a $25 entry fee into the park

Average winter temperatures: Daytime highs in the 60’s to low-40’s at night

What you need to know: This is the main campground for the Organ Pipe Cactus National Monument. The area is surrounded by desert plants and cacti and has numerous hiking trails.

CALIFORNIA

Joshua Tree National Park

https://www.nps.gov/jotr/planyourvisit/jumbo-rocks-campground.htm

Jumbo Rocks Campground

Twentynine Palms, California

Cost: $20 per night plus entrance fee

Average winter temperatures: Daytime temperatures average 60 degrees with freezing nights

What you need to know: There are several campsites at Joshua Tree National Park. The Jumbo Rocks is centrally located and offers beautiful views of the rock formations. The park is known for hiking, climbing, and stargazing. Pets are not allowed on trails. Make your reservation early; the park is busiest during February and March.

FLORIDA

Everglades National Park

https://www.nps.gov/ever/planyourvisit/camping.htm

Homestead, Florida

Cost: Starting at $33 a night

Average winter temperatures: Range from high 50’s to high 70’s

What you need to know: This park features towering Cyprus trees and an abundance of animals who call the Everglades home. Choose from front country and wilderness back country campsites, the latter reached mostly by canoe, kayak, or motorboat. Reserve early as this park is busiest from November through April.

GEORGIA

Reed Bingham State Park

https://gastateparks.org/ReedBingham

Adel, Georgia

Cost: From $35 per night plus $5 parking fee

Average winter temperatures: Low 40’s to mid-60’s

What you need to know: This park features a 375-acre lake, and there are rentals for canoes and kayaks. Visitors also enjoy fishing, birding, and hiking. There is abundant wildlife, including tortoises, snakes, alligators, and nesting bald eagles. During the winter, thousands of black vultures and turkey vultures make their home here.

LOUISIANA

Grand Isle State Park

https://www.lastateparks.com/parks-preserves/grand-isle-state-park

Jefferson Parish, Louisiana

Cost: Starting at $18 per night plus $3 per person admission fee

Average winter temperatures: mid-40’s to mid-60’s

What you need to know: This park offers fishing, birding, crabbing, hiking, and boating throughout the lagoons and the Gulf shore. There is a toll bridge to get to this state park. While the park is open, the boardwalks are currently closed due to damage from Hurricane Ida and campsites are limited.

NEVADA

Valley of Fire State Park

https://parks.nv.gov/parks/valley-of-fire

Overton, Nevada

Cost: $20 per night for Nevada residents and $25 per night for non-Nevada vehicles, an additional $10 for utility hookups (WiFi for an additional fee)

Average winter temperatures: Can range from freezing to 75 degrees so pack accordingly

What you need to know: This 40,000-acre park is known for its bright red Aztec sandstone and its ancient, petrified trees and petroglyphs dating back more than 2,000 years.

OREGON

Harris Beach State Park

https://stateparks.oregon.gov/index.cfm?do=park.profile&parkId=58

Brookings, Oregon

Cost: Starting at $20 per night for residents (non-residents pay 25% more)

Average winter temperatures: Mid-50’s in the day to low-40’s at night

What you need to know: While winter is not beach weather, this park includes a beautiful beach for strolls, as well as walking paths and hiking trails. There are tent sites, RV sites, and yurts. Some of the campsites are closed during the winter so please check before you book.

SOUTH CAROLINA

James Island County Park

https://ccprc.com/68/James-Island-County-Park

Charleston, South Carolina

Cost: Starting at $35 per night campgrounds and cottages are available

Average winter temperatures: Mid-40’s to low-60’s

What you need to know: The 643-acre park features open meadows and miles of paved trails for walking, biking, and skating. While the Splash Zone is not in operation during winter months, there is a climbing wall and disc golf course. Not only is the park pet-friendly, it also features a dog park.

TEXAS

Enchanted Rock State Natural Area

https://tpwd.texas.gov/state-parks/enchanted-rock

Fredericksburg, Texas

Cost: Starting at $14 per night plus a day pass fee of $8 per person; no RV or vehicle camping

Average winter temperatures: Daytime highs of mid-60’s to nighttime lows of low-40’s

What you need to know: The park features a huge pink granite dome that gives it its name. There is 1,600 acres of desert landscape, including opportunities for hiking and rock climbing. Pets are limited to one trail, and there is no bike riding on any trails.

UTAH / COLORADO

Dinosaur National Monument

https://www.nps.gov/dino/index.htm

Jensen, Utah

Cost: Camping starts at $0 in the backcountry and ranges from $6-$40 at other sites plus an entrance pass ranging from $15-$25

Average winter temperatures: Elevations in the park may influence temperatures which can fluctuate from 0 degrees to 30 degrees in January. Pack accordingly.

What you need to know: This is your chance to camp where dinosaurs once roamed. The park covers 210,000 acres at the intersection of Utah and Colorado, and offers hiking, river rafting, and petroglyph viewing. Six campgrounds provide a variety of options. Not all are open in the winter. There are places where pets are permitted and where they are not.

Do you have a favorite winter camping spot? Share it in the comments.

This article is furnished by California Casualty, providing auto and home insurance to educators, law enforcement officers, firefighters, and nurses. Get a quote at 1.866.704.8614 or www.calcas.com.

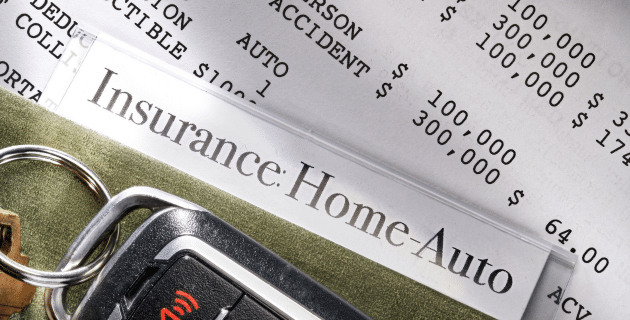

by California Casualty | Auto Insurance Info, Finances, Homeowners Insurance Info |

Insurance policies may seem like they’re written in another language. Yet it’s important to understand the terms so you can get the most out of your coverage. Here’s a quick tutorial on deductibles and what they mean for your auto and home insurance.

What is a deductible?

Simply put, a deductible is the amount of money that you pay out-of-pocket before insurance kicks in. Generally, your insurer deducts the deductible amount from the payment that they make on your claim. You can find the deductible listed on the declarations page, which is the front page of your policy.

Example: If the cost of a repair is $1,500 and your deductible is $500, insurance will cover $1,000.

Unlike health insurance deductibles, you do not have to reach an annual amount in an auto or home policy before insurance will pay. Each time you file a claim, there is a deductible (if it applies). One exception is the state of Florida where hurricane deductibles are once per season.

High vs. Low Deductibles

You select your deductible from a range of choices provided by your insurer. If you choose a lower deductible, that means your insurer will need to cover more in the event of a claim, which will raise the cost of your policy. If you choose a higher deductible, you’re willing to cover more of the cost in a claim, and that will lower your premium.

Lower deductible = Higher insurance premium

Higher deductible = Lower insurance premium

It’s important to note that you will have to pay the deductible if a loss occurs in a car accident, even if you think the other driver is at fault.

You may think twice about filing a claim for a damage amount that is close to your deductible. For example, if your deductible is $1,000 and repairs are $1,250, it may not be worth it. You’d be responsible for the bulk of the repairs, and by filing a claim, your rates may go up when you renew. See our blog about when you need to file a claim and when you don’t.

There are different types of coverage available to you for your vehicle. Some may be mandated by your state or your lender, and others are optional. Not all coverages carry a deductible.

The following coverages include a deductible, and you may choose a different deductible amount for each one:

- Collision: This coverage kicks in when you collide with another car or object.

- Comprehensive: This coverage is for damage from other causes such as hitting a deer or having a tree fall on your car.

- Uninsured motorist property damage (UMPD): This coverage is for property damage from accidents with another driver who is uninsured and at fault. UMPD may or may not have a deductible; it depends on the state and the type of loss. (Uninsured motorist coverage, which is different than UMPD, does not have a deductible.)

- Personal injury protection (PIP): This coverage pays for medical expenses regardless of who is at fault.

Pro Tip: Being able to set a deductible for each type of coverage allows you to assess the likelihood of your needing that coverage. For example, if you live in the country and might be more likely to encounter a deer than another car, you can lower the deductible for comprehensive and raise the deductible for collision.

There is auto coverage that does not carry a deductible, and that’s liability coverage. With liability coverage:

- If you are at fault: You hit another car and cause property damage and/or driver injuries. Your liability covers the damage to the other driver and his/her car without requiring a deductible. However, your own collision policy pays for damage to your car, which would come with a deductible.

- If someone else is at fault: Another driver hits your car and/or injures you. Their insurance will pay for damages and medical expenses. There are no deductibles.

Your insurer can provide quotes for different levels of deductibles and work with you to determine the best coverage for your budget.

Homeowner’s Policies and Deductibles

Whether you’re buying a new home, or you’ve owned yours for years, your homeowner’s policy protects your investment. Costs vary by location, age of home, construction type, number of bathrooms, and many other factors.

With homeowner’s insurance, there are generally three choices for deductibles:

- Flat deductibles: You would choose a fixed dollar amount, such as $1,000. That is the amount you would pay out-of-pocket before insurance kicks in.

- Percentage deductibles: You would choose percentage of your Coverage A limit. If your policy covers your home at $300,000, and you choose a 2% deductible, you would be responsible for 2% of $300,000 or $6,000.

- Peril-specific deductible option: You could have a flat deductible amount and then carry a different one specifically for wind/hail losses.

There are coverages under your home insurance that do not carry a deductible. These include Scheduled Personal Property (SPP) Coverage, Coverage E: Personal Liability, and Coverage F: Medical Payments to Others.

- Scheduled personal property (SPP) Coverage is for items that have higher values above your personal property coverage limits. This includes heirlooms, watches, jewelry, instruments, furs, or anything about which you are especially concerned such as a special guitar. (Musical instruments for example do not have a contractual limit but you will want to schedule an instrument that is special to you.) SPP offers much broader coverage for your precious items – if you lose a set of earrings, they are covered; if a diamond falls out of a ring, or if a guitar falls off a shelf and gets stepped on, they’re covered. There is no deductible if the covered items are stolen, lost, or damaged. Insurance pays the lowest of the four options: repair, replace, actual cash value or the amount of insurance.

- Personal Liability protects you if a claim is made or a suit brought against you for bodily injury or property damage caused by an occurrence to which coverage applies. These are expenses paid to third parties for their injuries and damages. Liability covers you at your place or anywhere in the world. If you are found liable, the policy will pay up to its limit of liability for damages for which an insured is legally liable. This can include medical expenses, lost wages, pain and suffering, and permanent scarring. The policy also provides a defense in court, if needed, for the policyholder. This is at the insurance company’s own expense.

Insurance may seem complicated, but it doesn’t have to be. Your agent can answer any questions you may have. Contact your insurer to find out more about protecting your most valuable possessions.

This article is furnished by California Casualty, providing auto and home insurance to educators, law enforcement officers, firefighters, and nurses. Get a quote at 1.866.704.8614 or www.calcas.com.