by California Casualty | Calcas Connection, Good to Know |

Seeing a wall of flames or a madly spinning tornado bearing down on your community or neighborhood is the worst time to wonder, “Do I have enough insurance to build my home again?”

Seeing a wall of flames or a madly spinning tornado bearing down on your community or neighborhood is the worst time to wonder, “Do I have enough insurance to build my home again?”

While some areas of the country have already experienced tornadoes and record flooding, fire and storm season is just beginning.

We’ve seen enough disasters to know the stress and financial impact they leave behind. More out-of-control fires and powerful storms have resulted in higher cleanup costs, elevated rebuilding prices and shortages of manpower and materials, due to the damage in a concentrated area.

It’s very important to make sure that you have enough insurance for your home and property.

Here’s why:

- Half of American homeowners have told experts that they don’t really know what their homeowners insurance policy covers

- Other studies estimate that six out of ten homeowners are underinsured by an average of 20 percent – meaning if their house costs $200,000 to replace, they would fall short by about $40,000 if they had a total loss

- Less than 20 percent of those in flood or earthquake-prone areas have flood or earthquake insurance

Here are some of the factors that could lead to a home being underinsured:

- Improvements and upgrades. When you buy new appliances, remodel kitchens and bathrooms or add on to your home, those improvements may not be covered by your original insurance policy.

- Hazardous materials removal costs. After a disaster, your property may be full of dangerous chemicals, asbestos and other hazardous materials. It may take months to get proper permits, and the costs to remove the toxic residue can be quite high.

- Rising construction costs. After large-scale disasters, building materials, construction crews and equipment may be in short supply. Costs in many areas have skyrocketed after massive property destruction.

- Updated building codes. Rebuilding an older home to meet today’s safety codes may be expensive, especially if you bought your home decades ago.

- Limited loss of use coverage. Make sure you have enough coverage to pay for extra living expenses (rent, food and other essentials) while your home is rebuilt or repaired. It’s important to factor in extended time after large disasters, sometimes more than a year.

- Not enough personal property protection. Make sure that you have enough contents coverage to replace the many items you own – bedding, clothing, kitchen items and electronics. Don’t forget scheduled personal property for high value items, such as jewelry, special musical instruments, fine art and collectibles.

Being Prepared

A yearly policy review is a must. As your insurance partner, it’s imperative that you tell us about any home improvements/upgrades that you’ve made. A California Casualty advisor will take the time to explain your policy and help make sure that you have the coverage you need with the discounts you deserve.

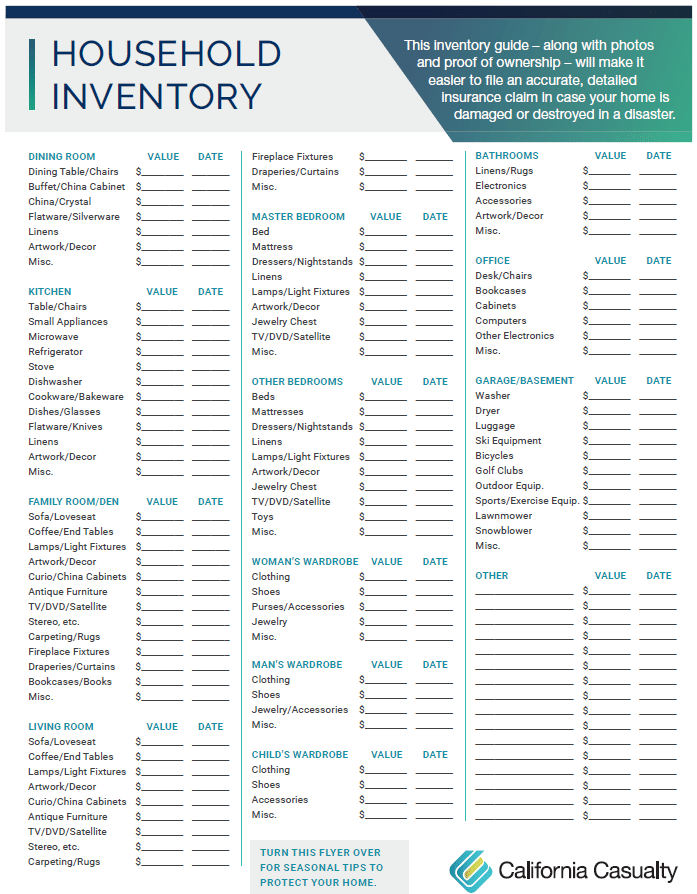

Its’s also important that you make an inventory of your possessions. Not only will it help determine the amount of coverage you need, but it speeds up the process of replacing those items. Only half of American homeowners and renters have done an inventory, which could leave them in the lurch after a disaster.

TAKEAWAY:

Take a moment and contact one of our customer service representatives for your policy review by calling 1.800.800.9410, option 3.

by California Casualty | Homeowners Insurance Info |

Odds are you or someone you know is getting married. June through September is the peak of the wedding season in the United States. Every year, 2.1 million couples tie the knot, which breaks down to nearly 6,000 weddings a day. But what happens if the groom gets food poisoning the night before the wedding or a fire burns down the reception hall? Believe it or not, there is insurance for that.

Wedding insurance typically runs from $155 to $550 dollars, depending on how elaborate your special plans might be. It covers the cost to reschedule the nuptials due to weather, injury, the wedding dress or tuxedos not showing up, the failure of a caterer, or if the location is unable to host your event. You can also insure the wedding rings, presents and the photographs.

Is wedding insurance worth it? One provider researched claims filed between 2011 and 2015 and found:

- Problems with vendors (venue went bankrupt, photographers failing to deliver and DJs not showing up) accounted for 30 percent of payments

- Illness and injury resulted in 29 percent of the claims

- Weather issues caused 16 percent of the cancelations

- Military deployment was the cause for 10 percent

The good news is that once the rings are exchanged and the honeymoon is over, there are important insurance decisions to make, some that could save you money.

- Marriage Discount

Most auto and home insurance companies offer discounts for newlyweds. This applies to both men and women; however, men under the age of 25 see the biggest savings since they are usually considered high risk drivers. The lower rates can also apply to those in domestic partnerships.

- Combining Autos

If you both have separate cars with different insurance companies, now that you are married you can save money by putting both vehicles on the same policy. Most insurance companies give discounts for multiple vehicles. It will also ensure that both drivers are covered no matter which car they use. You can find more savings by bundling your auto with your homeowners or renters insurance.

- Increase Homeowner or Renters Coverage

You didn’t buy them, but all those wedding presents are valuable. You now have a new set of china, expensive new appliances and other things for your home. These assets need to be covered. Talk to an insurance advisor to make sure you have enough coverage to protect all the things you own and to increase your liability protection. If you rent, keep in mind that your landlord’s insurance does not cover your possessions and you need renters insurance to be certain you’ll be reimbursed if a fire or broken pipe in the unit above damages your furniture, appliances and electronics, not to mention all your clothes. Renters insurance will also pay for living expenses while the home or apartment you rent is repaired, and pays for any medical bills or lawsuits if someone gets injured at your place.

While you are at it, this is also a great time to create an inventory of all the things you own to help you purchase the right insurance protection and make filing a claim much easier.

- Get Extra Protection for High Value Items

That beautiful new wedding ring and special gifts like fine art, china or silverware may need scheduled personal property protection, often called a “floater,” to make sure they are covered for their full value. Most homeowners and renters policies will only provide limited coverage for those high value items. Scheduled personal property coverage will also pay to replace a ring, without a deductible, even if it was misplaced or damaged in the disposal.

by California Casualty | Homeowners Insurance Info |

Your budget may already be on life support if you are getting married. The average cost of a wedding in the United States is now over $30,000 and climbing. I cringe to think of what tying the knot will cost when my daughter finally meets the man of her dreams and there is a proposal.

The costliest weddings are in in Manhattan, where the average bill soars to over $88,000. The average where I live (Colorado) is around $32,000.

Renting the venue and paying for the reception was the biggest expense, averaging almost $15,000. The wedding ring and other jewelry came in at $5,800.

If you are planning a wedding (or a father taking a loan to pay for one), here are some ideas for reducing the stress and the expense of saying, “I do.”

- Pare down the guest list. The average cost per guest is around $200. Times that by 100 and you’ve already hit $20,000. It’s a hard task cutting the invites but it could save you thousands of dollars.

- Pick a less expensive place for the reception. Instead of a fancy downtown hotel, consider a meeting hall. Having it at a restaurant will also save tons on catering, rental and alcohol. You can really cut your costs and use a friend’s or relative’s home.

- Reduce your flower costs. Fresh flowers are beautiful, but like memories, they fade and wilt. Choose flowers that are local and in season. Even though you might have fewer flowers, most people won’t notice.

- Simplify your menu. Hors d’oeuvres and cocktails cost less than a five course sit-down meal. A nice compromise is a buffet luncheon or dinner.

- Schedule your wedding in the off season or on a weekday. Weekends from June through September, when most weddings occur, will cost more. You’ll find better deals if you plan a wedding for the fall or winter months, except on Valentine’s Day.

- Create your own invitations. Instead of frilly paper and multiple ink colors, go simple to cut production, printing and mailing costs.

- Hire a DJ instead of a band. Many couples on a budget also make their own mix-tape or iPod play list.

- Let your guests help with wedding photos. Hire a photographer for the special portrait and family shots, but purchase some low end digital or disposable cameras for capturing the reception. You will be amazed at the pictures your friends and relatives will take for you.

- Get a smaller cake. Forget expensive tiered cakes with fancy frostings, order fabulous sheet cakes that can taste just as good but cost much less and are easier to serve. Some couples have opted for cupcakes, pies, or desert bars with chocolate fountains instead of the cake.

Here’s one final money savings tip: don’t mention you are taking estimates for a wedding. Many vendors charge more for weddings than other events. Instead, say you are planning a family party and you could save anywhere from 20 to 40 percent.

Tie up your insurance.

Once the rings are exchanged and the honeymoon is over, there’s another important step – getting your auto and home insurance in order. Here’s a checklist for newlyweds that can also save you money.

- Combine Your Insurance

If you have separate cars with different insurance companies, now that you are married you can find discounts by putting both vehicles on the same policy. It will also ensure that both drivers are covered no matter which car they use. Get extra savings by bundling your autos with your home or renters insurance.

- Marriage Discount

Make sure to inform your insurance company that you got married – most auto and home insurance companies offer important discounts for newlyweds. Men under the age of 25 are usually considered high risk drivers. However, once they marry they often see a big drop in insurance premiums. The lower rates can also apply to those in domestic partnerships.

- Increase Homeowner or Renters Coverage

Wedding presents are wonderful. You now have a new set of china, expensive new appliances and other things for your home. These assets need to be covered. Talk to an insurance advisor to make sure you have enough coverage to protect all the things you own and to increase your liability protection. It’s also a great time to create an inventory of your possessions to help you purchase the right insurance protection and make filing a claim much easier.

- Get Extra Protection for High Value Items

That beautiful new wedding ring and special gifts like fine art or silverware may need scheduled personal property protection, often called a “floater,” to make sure they are covered for their full value. Most homeowners and renters policies will provide limited coverage for those items. Scheduled personal property coverage will also pay to replace a ring, without a deductible, even if it was misplaced or damaged in the disposal.

by California Casualty | Homeowners Insurance Info |

Springtime; for many of us it means we can start hanging up the cold weather gear and begin getting out the gardening equipment. However, the pleasant change in weather can often lull us into a false sense of security. In fact, I’m reminded of the warning Julius Caesar was given, “Beware the Ides of March.”

So what does that warning have to do with you and me? While March marks the end of winter, it starts a dynamic time of year with a clash of late season cold fronts and warm gulf air leading to dangerous thunderstorms, flooding and even tornadoes.

Many scientists warn that between climate change and El Nino, we are facing some of the most extreme and unpredictable weather patterns ever seen: one of the worst droughts and fire seasons ever in California followed by torrential rains and heavy snows, record flooding in Texas, Missouri and South Carolina, rare deadly December tornadoes across the Midwest and South and unprecedented holiday warmth in the Northeast.

Maybe we should change Shakespeare’s line to “Beware the Ides of Spring.”

Springtime Dangers

Flooding

Flood season begins in spring as winter snow and ice melt. Severe thunderstorms can add tremendous amounts of water to the runoff, often inundating cities and towns located in flood zones.

Flooding is the most common and costly natural disaster in the United States, causing an average of $50 billion in economic losses each year. Anyone living in a low-lying area near a lake, river or stream should make sure they are protected. Homeowners and renters insurance don’t cover floods from rivers, streams, or other runoff; if you want your home and valuables protected, you need flood insurance that often has a 30 day waiting period.

Flooding caused by a damaged roof or broken water pipe is covered by most homeowners insurance. While it can happen any time of year, springtime thawing can be the culprit. Do you have enough coverage if water should destroy your valuable possessions? The Federal Emergency Management Agency estimates that just two inches of water can cause more than $10,000 for repairs and replacement of flooded items. Six inches of water can add up to more than $30,000.

Fires

While a house fire can happen any time of year, spring marks the start of wildfire season. More than 4,600 structures were destroyed by wildfires in 2015, 2,667 of those were homes or apartments.

Fuels, such as grasses and brush, start to dry out as temperatures warm. Before they become a threat to your home you should mow and trim back any grasses, trees or bushes to create a 30 foot defensible space. Don’t forget to move gas grills, firewood and other combustibles 15 to 30 feet away from your home. You can find more wildfire prevention tips here.

Tornadoes

The volatile mix of warm and cold usually results in tornadic activity. Almost every state has experienced a tornado, and if you live in the South, Midwest or points east you may have already taken these tornado preparedness actions:

- Identify a safe place in your house (basement, storm shelter or sturdy interior reinforced room on the lowest floor of the home

- Prepare an emergency kit with first aid supplies, food, water and sanitary needs (include important medicines, eye glasses, etc.)

- Practice tornado drills

Severe Thunderstorms

Thunderstorms are the top cause of insured loss each year in the United States due to high winds, large hail and dangerous lightning. When a thunderstorm approaches, immediately move indoors and away from windows and avoid electrical equipment and corded telephones. Preparations for severe thunderstorms are much the same as tornadoes.

How to Protect Your Property

Before wild weather has a chance to threaten your home, here are some key tips to help prevent damage:

- Check roofs and shingles for damage, lifting or other signs that they might leak

- Clean gutters and drain spouts and make sure they direct water away from your home’s foundation

- Look for loose boards, cracking or other damage on decks and porches to avoid tripping, falls or other hazards

- Inspect the exterior of your home for cracks, holes or exposed wood or siding that could allow water, insects or small wildlife to get in

- Make sure chimneys and vents are well sealed and sturdy to prevent water or wind damage

- Trim back trees and bushes, looking for weak or broken branches or other damage, to protect against them falling into roofs or siding

Check Your Insurance

Before a catastrophe strikes, the Insurance Information Institute says you should:

- Purchase homeowners or renters insurance

- Get flood insurance if you live in a flood prone area

- Review your policy so you understand your coverages (replacement costs, replacement of personal possessions, and additional living expenses)

- Make a full inventory of everything you own

After a Disaster

If the unexpected should occur, you should take these steps:

- Secure your property from further damage or theft

- Contact your insurance company as soon as possible

- Catalogue your losses and take pictures

- Save receipts of meals, purchases and hotels while you are unable to live at home

- Be careful of fraudulent contractors

Now is good time to reevaluate your protection against the unpredictable moods of spring; contact a California Casualty advisor to purchase flood insurance, get a review of your policy or add any coverage that you might need. Give a call today at 1.800.800.9410 or visit www.calcas.com.

Resources for this article:

https://news.yahoo.com/record-el-nino-climate-change-drive-extreme-weather-170109695.html;_ylt=AwrTcdtKdZVWbA8ATzMnnIlQ;_ylu=X3oDMTBya2cwZmh2BGNvbG8DZ3ExBHBvcwM1BHZ0aWQDBHNlYwNzcg–

https://www.floodsmart.gov/floodsmart/pages/flooding_flood_risks/the_cost_of_flooding.jsp

https://www.calcas.com/documents/10326/0/wildfire_pamphlet_residential_CA.pdf/4c476835-55f4-4a70-a208-0f7930218e90

https://www.nifc.gov/fireInfo/fireInfo_statistics.html

https://www.redcross.org/prepare/disaster/tornado

https://www.iii.org/article/making-sure-your-home-properly-covered-disaster

https://www.redcross.org/find-help/disaster-recovery/recovering-financially

by California Casualty | Auto Insurance Info, Homeowners Insurance Info |

As we drop the confetti and toast the New Year, an annual tradition is to make a resolution. What will yours be? Here are the top five resolutions Americans have made in recent years:

- Lose weight

- Get organized

- Spend less and save more

- Enjoy life

- Become more fit and healthy

Unfortunately, research shows less than 10 percent of those of us who make resolutions actually keep them.

But, there are easy actions you can take that could save you money and provide peace of mind.

Every year, many Americans fail to take stock of their biggest assets: their homes and vehicles. Here is a list of 11 simple resolutions you can make this New Year to protect the most valuable possessions you have worked so hard to attain.

7 Home Insurance Resolutions:

- Do a yearly policy review with an insurance advisor to check that you are getting all the discounts you qualify for, that you adequately insure any new additions or appliances, and verify that your liability coverage isn’t lacking

- Make sure you have replacement value if a fire or other disaster strikes

- Purchase earthquake or flood insurance if you live in areas prone to either

- Save on your premiums by investing in security and fire suppression systems

- Get renters insurance if you don’t have it yet

- Protect high-dollar items such as jewelry, fine art or musical instruments with scheduled personal property insurance

- Complete a comprehensive inventory of everything in your home in case you should ever have a claim

4 Auto Insurance Resolutions:

- Get a yearly policy review to check deductibles, coverages and to make sure you are getting all the discounts you qualify for (professional, multi-policy, good student, mature driver)

- Make certain you have adequate protection from uninsured or under-insured drivers

- Add any new drivers to your policy (teens or a new spouse)

- Bundle your auto and home insurance to receive deeper discounts

We Are Here To Help

Start the New Year off right; resolve to call today to make sure you are getting the professional discounts you deserve: $500 coverage for items destroyed or stolen from your vehicle, deductible waived or reduced if your vehicle is vandalized or hit while parked where you work, and special coverages for the equipment used for your job.

California Casualty advisors are ready to help you with any questions, do a policy comparison or review, or make any insurance changes you may need at 1.800.800.9410, or go online at www.calcas.com.

Resources for this article:

https://www.statisticbrain.com/new-years-resolution-statistics/

https://www.insurancejournal.com/news/national/2014/08/12/337407.htm

https://www.knowyourstuff.org/iii/login.html

{kind=link}