You may believe that everything in or around your home is covered by your homeowner’s policy, but that may not be the case. Sure home insurance will help you rebuild if there’s a fire, tornado. or a tree falls onto your home, but are you aware of what your insurance doesn’t cover?

These are the 5 most common things not covered by most home insurance policies:

{kind=link}

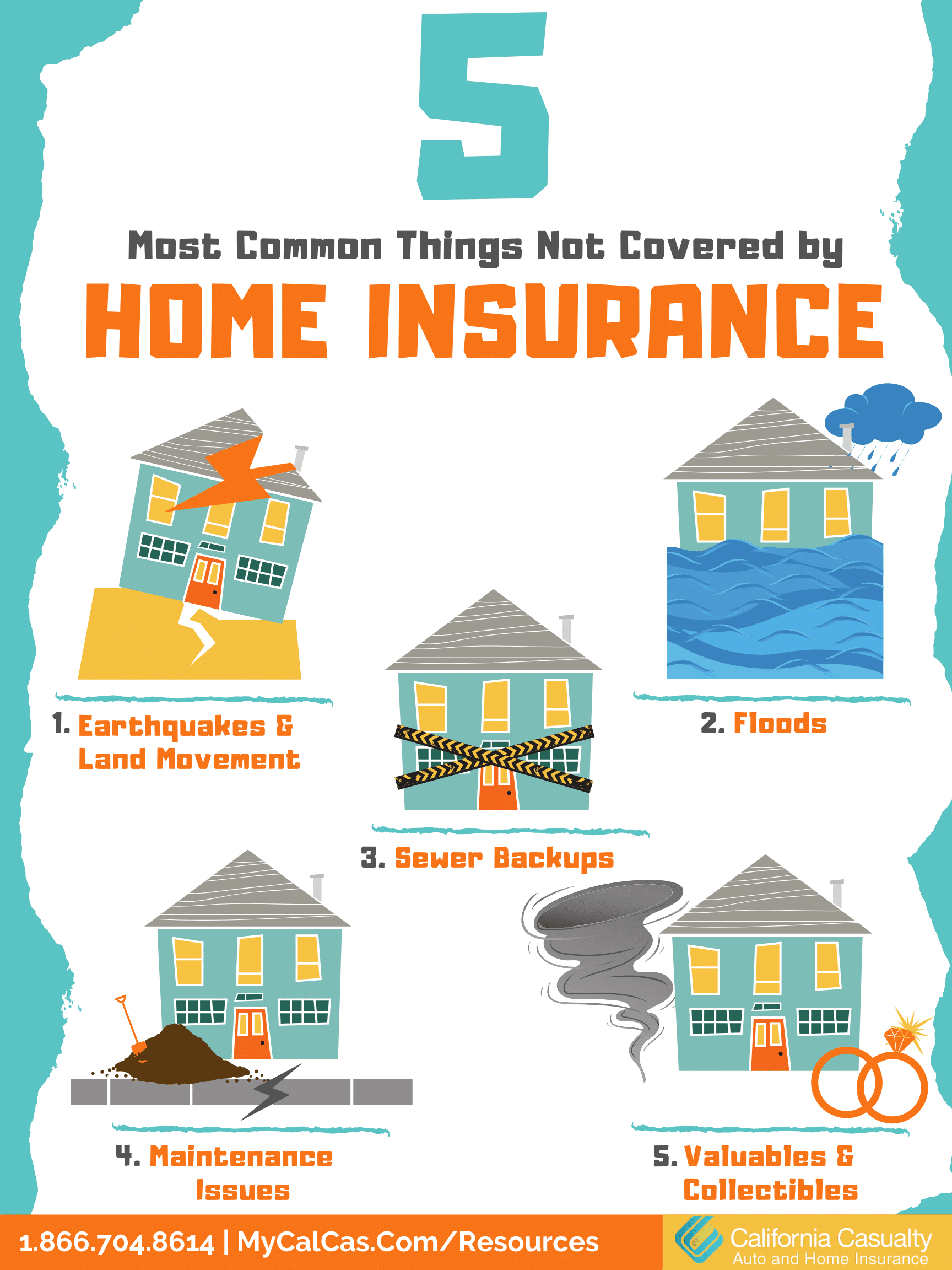

- Earthquake and Land Movement

- As landslides and earthquakes have become more common in many states, many people are surprised to learn that earthquake or land movement damage is not covered by standard homeowners insurance. You need to purchase separate earthquake and landslide insurance protection.

- Floods

- Multiple surveys have found a majority of homeowners and renters thought their property insurance protected them from flooding; it doesn’t. If you live in an area prone to flooding, consider purchasing flood insurance, provided primarily by the federal government. Keep in mind there is a 30 day waiting period before any flood policy can go into effect.

- Sewer Backups

- The sludge from sewer backup can do serious damage and make your home unsafe until it’s properly cleaned up, but it’s not covered under most homeowner insurance policies. Your insurance company can provide a special endorsement to cover sewer or sump pump backups. What you may not know is that homeowners are responsible for the maintenance of sewer and water lines through their property up to the sewer main, and many cities and utility departments will deny responsibility for most sewer incidents.

- Maintenance Issues

- Insurance companies can dispute payment of damage or injuries if you fail to repair a broken step or other obvious hazards, or for mechanical breakdown of an appliance. In most cases, you will also need a special rider to cover food that might be lost due to a power outage or failure of a freezer or refrigerator.

- Expensive Jewelry, Fine Art, Firearms, Musical Instruments, Furs, and Collectibles

- Many people learn after a fire or tornado that their precious items only had minimal coverage. You’ll need special scheduled personal property coverage, often called a “floater,” to make sure they are protected for their full value. In fact, 60 percent of homeowners have not documented all the valuable things they own. What does that mean to you? Completing a home inventory can speed up your claim and help you determine how much coverage you need. Download our easy Home Maintenance Checklist, and stay prepared for a disaster before it’s too late.

For more information on what home insurance does cover, visit our website at www.mycalcas.com/home-insurance

Related Articles:

Flood Insurance is a Necessity Everyone Should Consider

Know Your Insurance: Climate Change Protection

This article is furnished by California Casualty, providing auto and home insurance to educators, law enforcement officers, firefighters, and nurses. Get a quote at 1.866.704.8614 or www.calcas.com.

- Educators Receive $1,000 Athletic Grants from California Casualty - May 22, 2024

- Music & Arts Grant Recipients – 2023 - December 1, 2023

- How to Tell When You Need New Brakes - November 20, 2023