Seeing a wall of flames or a madly spinning tornado bearing down on your community or neighborhood is the worst time to wonder, “Do I have enough insurance to build my home again?”

Seeing a wall of flames or a madly spinning tornado bearing down on your community or neighborhood is the worst time to wonder, “Do I have enough insurance to build my home again?”

While some areas of the country have already experienced tornadoes and record flooding, fire and storm season is just beginning.

We’ve seen enough disasters to know the stress and financial impact they leave behind. More out-of-control fires and powerful storms have resulted in higher cleanup costs, elevated rebuilding prices and shortages of manpower and materials, due to the damage in a concentrated area.

It’s very important to make sure that you have enough insurance for your home and property.

Here’s why:

- Half of American homeowners have told experts that they don’t really know what their homeowners insurance policy covers

- Other studies estimate that six out of ten homeowners are underinsured by an average of 20 percent – meaning if their house costs $200,000 to replace, they would fall short by about $40,000 if they had a total loss

- Less than 20 percent of those in flood or earthquake-prone areas have flood or earthquake insurance

Here are some of the factors that could lead to a home being underinsured:

- Improvements and upgrades. When you buy new appliances, remodel kitchens and bathrooms or add on to your home, those improvements may not be covered by your original insurance policy.

- Hazardous materials removal costs. After a disaster, your property may be full of dangerous chemicals, asbestos and other hazardous materials. It may take months to get proper permits, and the costs to remove the toxic residue can be quite high.

- Rising construction costs. After large-scale disasters, building materials, construction crews and equipment may be in short supply. Costs in many areas have skyrocketed after massive property destruction.

- Updated building codes. Rebuilding an older home to meet today’s safety codes may be expensive, especially if you bought your home decades ago.

- Limited loss of use coverage. Make sure you have enough coverage to pay for extra living expenses (rent, food and other essentials) while your home is rebuilt or repaired. It’s important to factor in extended time after large disasters, sometimes more than a year.

- Not enough personal property protection. Make sure that you have enough contents coverage to replace the many items you own – bedding, clothing, kitchen items and electronics. Don’t forget scheduled personal property for high value items, such as jewelry, special musical instruments, fine art and collectibles.

Being Prepared

A yearly policy review is a must. As your insurance partner, it’s imperative that you tell us about any home improvements/upgrades that you’ve made. A California Casualty advisor will take the time to explain your policy and help make sure that you have the coverage you need with the discounts you deserve.

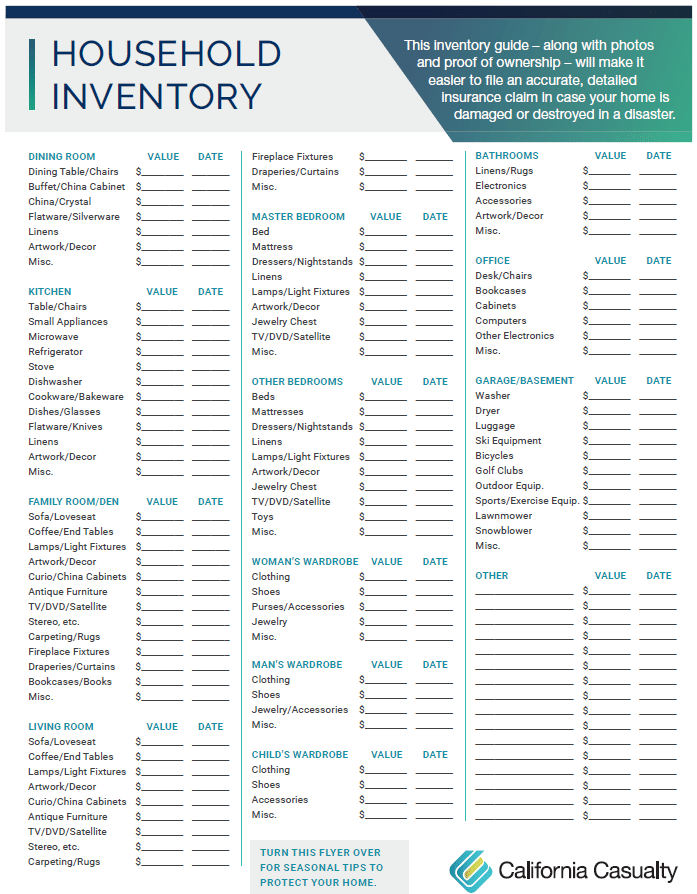

Its’s also important that you make an inventory of your possessions. Not only will it help determine the amount of coverage you need, but it speeds up the process of replacing those items. Only half of American homeowners and renters have done an inventory, which could leave them in the lurch after a disaster.

{kind=link}

TAKEAWAY:

Take a moment and contact one of our customer service representatives for your policy review by calling 1.800.800.9410, option 3.

- California Casualty Earns Financial Stability Rating® of A, Exceptional, From Demotech, Inc. - April 28, 2025

- Music & Arts Grant Recipients – 2024 - December 13, 2024

- Understanding Auto and Home Insurance Rate Changes - December 3, 2024

Thank you for the article on not having enough insurance. It was very helpful as well as customer service was in assisting me.